AI Agents Have Wallets Now. Liability Still Needs Proof

Good Proof by Mind Chill·25 February 2026·6 min read

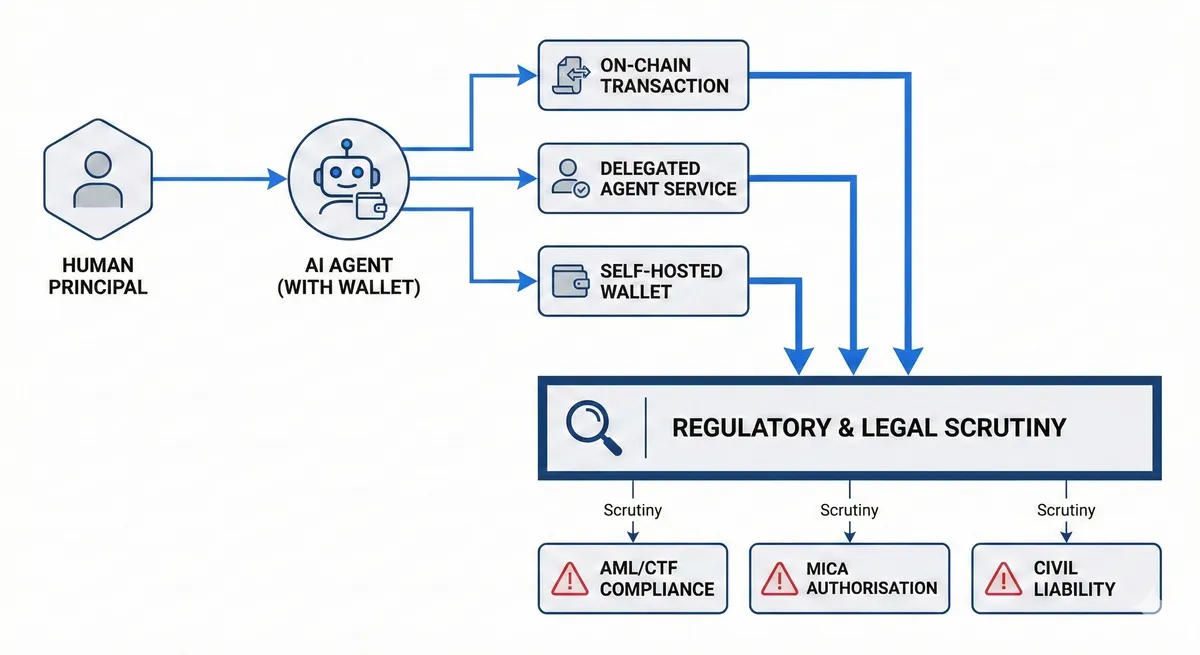

Agent wallets are moving from demos to production. The hard part is no longer making an agent transact. It is proving who authorised the action, what controls applied, and whether reliance should have stopped when conditions changed.

The legal frontier is not the wallet. It is the argument afterwards.

This week, a major industry discussion landed in plain English.

AI agents are being given crypto wallets so software can hold assets, pay for services, trade tokens, and even hire other agents. The technical pieces are falling into place. The legal ones are not

That is the real story.

Not that agents can transact.

That the world is about to get a new kind of economic actor, and the accountability model is still undefined.

In the meantime, regulated firms still have a problem.

Because when money moves, regulators and customers do not accept "the agent did it" as a defence.

They ask a much older question:

Who authorised this, under what rules, with what limits, and can you prove it?

This is already shipping, not theory

Wallet infrastructure is now being marketed and documented specifically for autonomous agents, including capabilities like spending, trading, and paying for services with built-in controls. :contentReference[oaicite:1]{index=1}

Once something is packaged as developer infrastructure, it stops being a concept and becomes a deployment pattern.

Which means the next bottleneck is not "can an agent pay?"

The bottleneck is:

Can an institution safely rely on what the agent pays, and defend that reliance later?

The uncomfortable reality: obligations do not disappear when the click disappears

Agentic wallets compress decision time.

Compliance does not compress with it.

In the EU, the Travel Rule regime for crypto-asset transfers is no longer an emerging topic. The EBA Travel Rule Guidelines apply from 30 December 2024 and explicitly tell PSPs and CASPs to set out and keep up to date policies and procedures for determining what information should accompany transfers and how they establish their role in a transfer chain. :contentReference[oaicite:2]{index=2}

So the question becomes operational:

When an AI agent initiates or routes transfers, who is accountable for ensuring the right information and controls were applied at the moment of execution?

Answer: the firm still is.

The firm just now needs a stronger proof layer, because the decision and the transaction can happen faster than internal governance can follow.

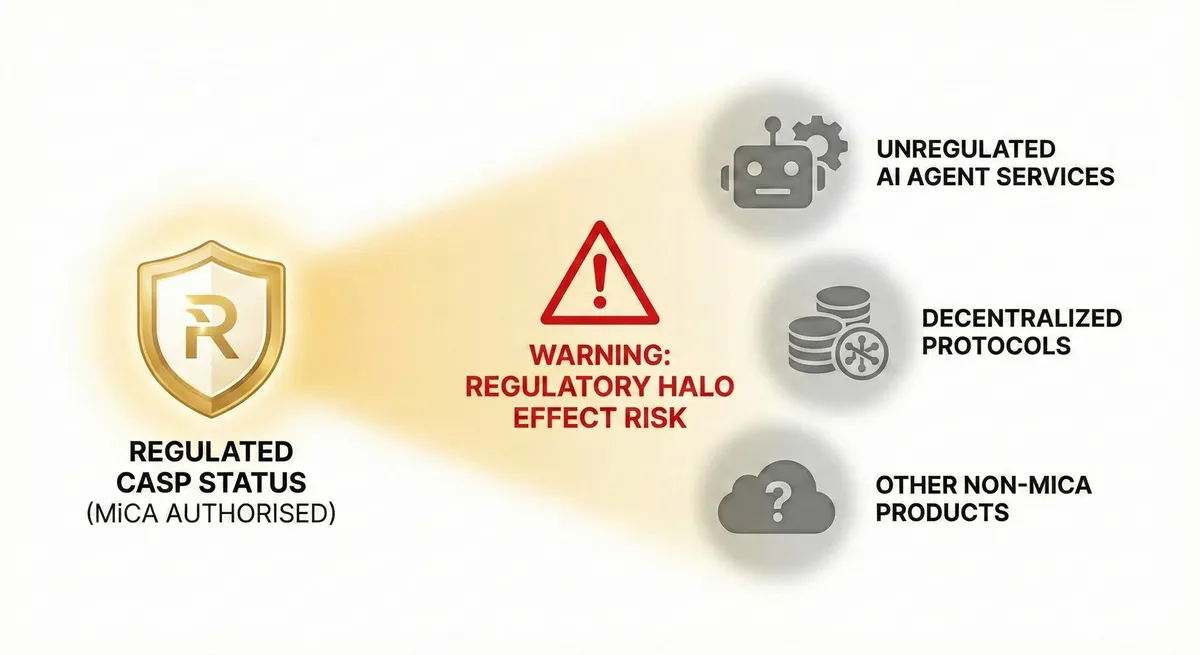

The MiCA problem agent wallets make worse: the halo effect

MiCA authorisation does not magically regulate everything a group offers.

ESMA explicitly warned that an authorised CASP status may create a "halo effect" that can mislead clients into thinking unregulated products or services offered through the same platform are also covered.

Agentic finance increases this risk because it makes product boundaries easier to blur:

one agent interface

one wallet

one set of actions

multiple regulatory scopes underneath

When a customer challenge arrives, firms will need to prove, per action:

which service scope applied

which protections applied

which disclosures applied

which controls applied

and why reliance was reasonable at that time

Without that, the firm is left arguing platform intent instead of proving decision reality.

The three failure modes buyers will pay to eliminate

If you sell into crypto capital markets, exchanges, custody, fintech rails, or regulated CASPs, these are the lanes where budgets show up quickly.

1. The self-hosted address problem

An agent sends funds to a self-hosted address.

Later, the transfer is flagged, challenged, disputed, or escalated.

The expensive question is not "did the transaction occur?"

It is:

what policy required what checks

what information was present at execution time

what risk classification was applied

who authorised the agent permission for that class of transfer

what limits were in force

whether conditions changed later that should have triggered stop-rely behaviour

Travel Rule policy expectations already exist, and the pace of transfers is only increasing. :contentReference[oaicite:4]{index=4}

2. The delegated agent chain problem

An agent pays another agent or service.

That service subcontracts again.

Now you have an onchain version of outsourced operations.

When something breaks, buyers will be asked to show:

who approved delegation

whether delegation was in scope

what spending limits applied

what monitoring and escalation existed

what the firm did when risk changed

This is where "agent autonomy" becomes "outsourcing without paperwork" unless you build proof into the workflow.

3. The authority and consent problem

When an agent transacts, the central question becomes whether the principal gave valid authority for that specific action.

This is not a philosophical debate.

It is the difference between:

a controlled transaction

and an unauthorised transaction that becomes a complaints and liability event

The first company that can prove per-action authority at scale will not just be safer.

It will be easier to approve internally, easier to work with externally, and faster to grow.

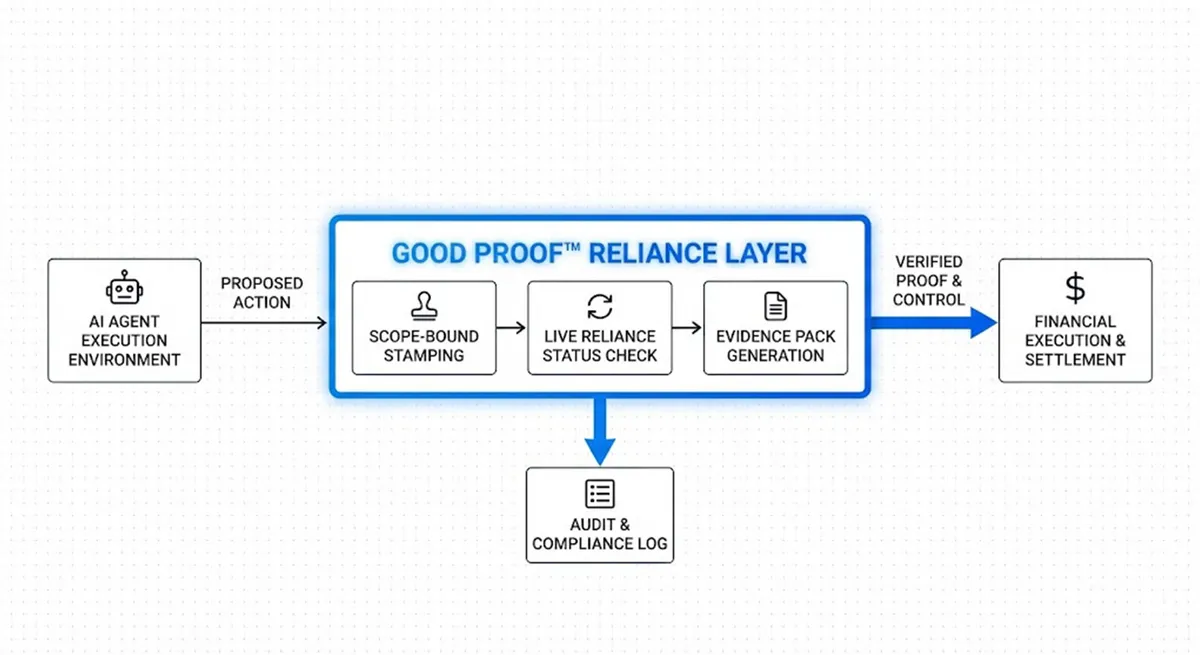

What Good Proof™ changes

Good Proof™ is not another wallet.

It is not an agent framework.

It is the missing reliance layer that makes agentic actions defensible.

Good Proof™ turns an agent action into a provable decision event

For high-impact actions, Good Proof™ produces evidence that is built for review, not for screenshots:

Scope-bound authorisation for the action class

Decision-time proof of what controls and limits applied

Live reliance status that can change when conditions change

Withdrawal semantics so reliance can be stopped everywhere it is enforced

This is the difference between "we have logs" and "we can prove reliance."

Good Proof™ makes revocation operational

Most stacks can tell you what happened.

Very few can tell you whether you should still rely on it now.

Agentic finance makes that gap expensive because risk conditions move:

sanctions data updates

fraud signals update

policies update

vendor status changes

wallet posture changes

approvals are withdrawn

Good Proof™ makes reliance state visible so enforcement can stop when it should stop.

Good Proof™ gives proof without exposing payloads

Regulated buyers often cannot share raw internals widely:

proprietary strategies

fraud models

customer data

full orchestration traces

Good Proof™ is designed around proof, not payloads, so teams can demonstrate control integrity without oversharing.

That is what makes it usable in procurement, audit, legal, and counterparty diligence.

Why buyers will pay for this now

Because the spend is already happening, just inefficiently.

Agent wallets do not create new responsibilities.

They compress old responsibilities into faster decisions.

Budgets already exist across:

AML and financial crime operations

compliance and licensing readiness

risk and assurance

security and incident response

legal and disputes

customer complaints handling

vendor and third-party oversight

audit support

Good Proof™ reduces the cost that sits underneath all of them:

reconstruction and disagreement after the decision.

When a system can answer "what was authorised and why" quickly, organisations stop burning weeks on internal archaeology and start moving faster with permission.

The line that matters

Agents having wallets is not the disruption.

Agents having wallets without a proof layer is.

The winners in agentic finance will not only be the firms that let agents act.

They will be the firms that can prove those actions were authorised, in scope, and safe to rely on when scrutiny arrives.

That is the category Good Proof™ was built for.

Good Proof™ resources for buyer and technical review