The Most Expensive Part of Insurance AI Is the Argument Afterwards

Good Proof by Mind Chill·25 February 2026·10 min read

Insurance AI is moving fast, but the real cost is not model development. It is what happens later when a claims decision, fraud action, pricing outcome, or AI assisted workflow has to be defended across risk, compliance, audit, complaints, and regulators

Insurance AI Is Entering the Expensive Phase

Most insurance teams are no longer asking whether AI will be used.

They are asking how to scale it without creating a future dispute machine.

That shift matters.

The first phase of AI in insurance was about capability.

The second phase is about reliance.

Not whether a model can produce an answer.

Whether a business can safely act on that answer when the stakes are real.

In insurance, the stakes are always real.

A pricing action changes affordability.

A fraud block delays access.

A claims workflow changes outcomes.

A prioritisation rule changes who gets seen first.

An AI generated recommendation can move a customer journey in ways that are hard to unwind later.

This is where many AI programmes quietly become expensive.

Not in engineering.

In the argument afterwards.

The Hidden Cost Is Not the Model. It Is the Reconstruction

When an insurance decision is challenged, the pain is rarely technical.

It is organisational.

People scramble to reconstruct:

what happened

what policy or rule applied

what the system was allowed to do

which team approved the workflow

which version was live at the time

whether the decision should still be relied on now

what can be shared without exposing sensitive internals

That reconstruction cost shows up everywhere, just under different labels:

compliance review

complaints handling

Consumer Duty evidence

audit requests

legal escalation

incident response

vendor due diligence

regulator engagement

internal challenge from second line and boards

It looks like many problems.

It is usually one problem.

The proof layer is weak.

Why This Is Urgent Now

AI Is Already Deep in Insurance Operations

Insurance is already well past AI experimentation.

AI is now embedded across core activities like pricing, underwriting, claims, fraud detection, and service operations.

GenAI has accelerated the pace, but that has mostly increased urgency, not reduced complexity.

The practical result is simple.

AI governance is no longer a policy topic.

It is an operating model topic.

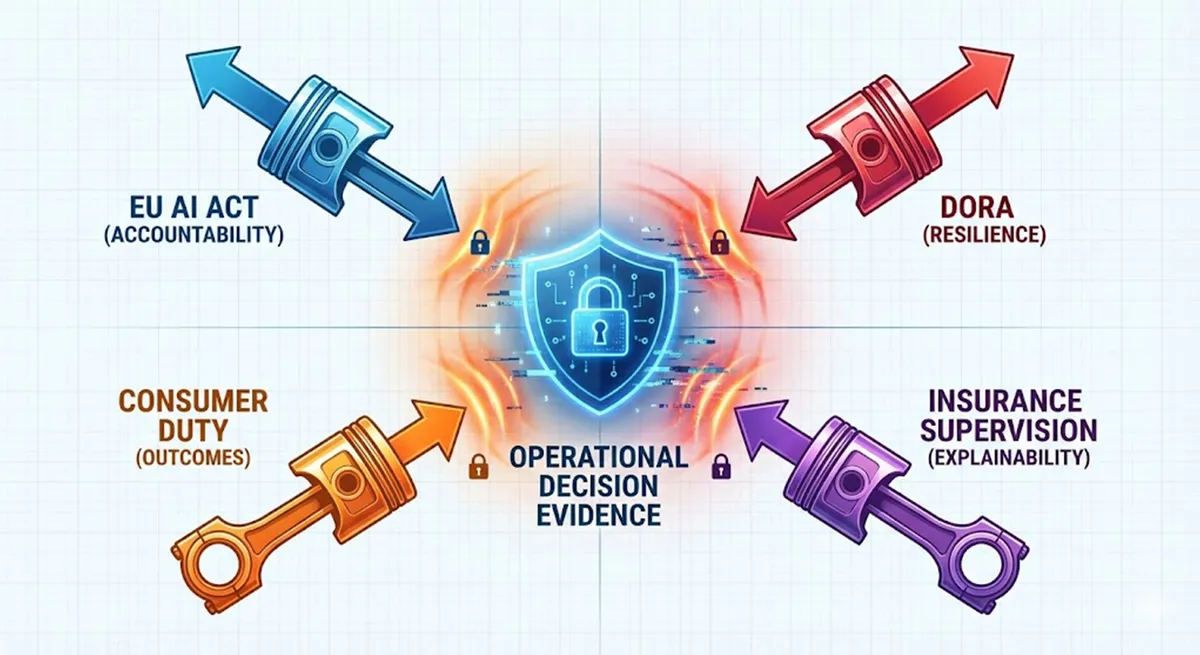

Regulation Is Shifting the Burden to Operational Evidence

The new pressure is not just to have policies.

It is to show that policies governed real decisions.

That is why the current regulatory mix matters:

EU AI Act pushes stronger expectations around risk management, documentation, logging, human oversight, and lifecycle accountability for high impact use cases.

DORA raises the bar on resilience and third party dependency management in ICT and AI heavy operating environments.

Consumer Duty in the UK reinforces outcomes evidence, not just process completion.

Insurance supervision is moving toward clearer expectations on fairness, explainability, record keeping, and oversight.

This is not a paperwork issue.

It is a decision evidence issue.

The Insurance Pain Point That Keeps Repeating

Insurance firms already have strong people, frameworks, and controls.

What they often do not have is a simple, portable way to prove reliance for specific AI assisted actions.

That creates repeated friction in five places.

1. Claims And Complaints

When a claims outcome is challenged, the question is rarely just whether a process was followed.

It is whether the insurer can show, clearly and defensibly:

what inputs and rules were relevant

what the AI assisted step did

what the human did

what policy and thresholds were in force

why the outcome was reasonable at that time

Without that, complaints and escalations become interpretation battles.

2. Fraud And Intervention Actions

Fraud pressure remains high.

The case for automation is obvious.

So is the governance burden.

Fraud controls need to be effective, but they also need to be challenge ready.

If an intervention is delayed, reversed, or disputed, the firm needs proof that survives scrutiny without exposing sensitive methods.

3. Consumer Duty Outcomes Monitoring

Consumer Duty raises the standard from reporting to evidence.

The difficult part is not collecting more dashboards.

The difficult part is proving that monitoring led to action, and that the evidence is clear enough for boards, risk teams, and supervisors to challenge and rely on.

That is where teams still lose time.

4. Cross Border AI Governance

For insurers operating across multiple markets, the challenge is not writing one policy.

It is proving that the same governance standard survives local workflows, vendors, and complaints processes.

This is where a portable proof layer becomes valuable.

It creates a consistent way to show decision integrity even when surrounding systems differ by market.

5. Third Party And Agentic Dependency Risk

Insurance is increasingly dependent on external ICT and AI providers.

That is no longer a procurement footnote.

As AI agents and orchestration layers become more common, the key question becomes:

which action relied on which service

under what conditions

with what status at the time

and how quickly reliance can be stopped if conditions change

That is a live control problem, not a static policy problem.

A Short Insurance Scenario That Makes The Problem Obvious

An AI assisted claims triage workflow flags a case for escalation and delay.

At the time, the action looks reasonable.

Three months later, the customer complains and the case is reviewed.

Now the organisation needs to prove:

which triage rule set was active

what signals were relied on

what the human reviewer saw

what policy thresholds applied

whether the approval state was valid at the moment of action

whether anything changed later that should have triggered review or withdrawal of reliance

Without a clear decision record, this becomes a cross team reconstruction exercise.

With a clear proof layer, it becomes a review.

That difference is where cost disappears.

Where Good Proof™ Fits

Good Proof™ is not another AI model layer.

It is not another governance dashboard.

It is not trying to replace underwriting, claims, fraud, GRC, or case management systems.

It sits underneath high impact decisions and makes them defensible.

Good Proof™ Turns Decisions Into Portable Proof

Most systems give you one of two things:

outputs

logs

Very few give you portable proof of reliance.

Good Proof™ is designed to do that.

It creates a verifiable decision layer around high impact actions so teams can prove:

what happened

what was authorised

what scope applied

what conditions were checked

what policy version or control state applied

whether reliance was valid at the time

whether reliance should later stop

That last point matters more than people think.

Good Proof™ Makes Revocation Operational

A lot of systems can tell you what happened.

Much fewer can help you answer whether you should still rely on it now.

In insurance, that distinction is critical.

Statuses change.

Controls change.

Approvals change.

Vendors change.

Risk posture changes.

Good Proof™ makes reliance status visible so teams can stop enforcement or dependencies when they should stop.

That is how a governance issue stays a governance issue instead of becoming a complaints issue and then a public issue.

Good Proof™ Supports Proof Without Payload Exposure

Insurance teams often face a false choice:

overshare internal logic and create risk

undershare evidence and create distrust

Good Proof™ is built around proof, not payloads.

That means teams can demonstrate decision integrity without exposing sensitive data, proprietary methods, or unnecessary internal detail.

This makes trust more portable across:

internal governance

audit

regulator engagement

third party review

partner and distribution relationships

Why This Gets Funded Faster Than Most AI Tooling

The biggest commercial mistake in this category is positioning.

Good Proof™ should not be framed as a brand new transformation budget.

It fits inside budgets that already exist because the pain already exists.

The Budget Holders Already Carry This Pain

Good Proof™ aligns naturally with workstreams that already have priority:

Responsible AI and AI governance

risk and compliance programmes

Consumer Duty outcomes monitoring

claims transformation and complaints reduction

fraud operations and investigation quality

internal audit and second line assurance

DORA and third party resilience

procurement and vendor assurance for AI and ICT providers

That is why the value story lands.

It removes delay and reduces repeated manual reconstruction across work that teams are already paying for.

It also reduces the risk of investing heavily in AI capability while leaving the decision evidence gap untouched.

A Practical First Deployment For Insurance Teams

The best way to start is not enterprise wide.

It is targeted.

Pick 2 to 4 high impact lanes where challenge, complaints, or scrutiny already create drag.

High Value Starting Lanes

Claims Decision Support And Exceptions

Focus on claim decline paths, exception handling, and AI assisted triage where outcomes need to be explainable and reviewable.

Fraud Flags And Intervention Actions

Focus on fraud blocks, escalations, or investigation triggers where teams need challenge ready evidence and controlled disclosure.

Pricing And Underwriting Governance Points

Focus on high impact pricing or underwriting decision points where governance and traceability matter most, especially where model outputs feed human decisions.

Third Party And Agentic Reliance Controls

Focus on decisions that depend on external AI or ICT services and need a live view of whether reliance is still valid.

What To Define In The First Sprint

For each lane, define a small but complete proof pattern:

The action class you are governing

The decision receipt fields that must exist

The scope and authority for who can rely on it

The status states and what changes them

The revocation or withdrawal triggers

The exception review path

The point is simple.

Do not start with a giant platform story.

Start where the argument cost is already visible.

Good Proof™ pays for itself fastest where disagreement is already expensive.

The Strategic Upside Is Bigger Than Compliance

The obvious value is auditability and control.

The bigger value is speed with permission.

Insurance firms are not short of AI ideas.

They are short of mechanisms that let risk, legal, operations, and leadership say yes with confidence.

When that confidence exists, firms can move faster on:

AI supported claims workflows

more responsive fraud operations

better customer support automation

controlled GenAI deployment

cross border governance consistency

vendor and third party integration

When that confidence does not exist, everything slows down and every pilot stays trapped in committee.

This is the quiet commercial role of Good Proof™.

It does not replace innovation.

It makes innovation easier to approve, safer to scale, and cheaper to defend later.

The Real Insurance Moat In The AI Era

As AI lowers the cost of building features, the scarce asset is no longer the interface.

It is the ability to create defensible reliance.

The winners in insurance will not be the firms with the most AI demos.

They will be the firms that can move fast and prove what they did when it matters.

That is the real moat.

Not the model.

Not the interface.

The ability to create defensible confidence at decision time and months later.

The Strategic Shift

Insurance does not need less AI.

It needs less ambiguity.

Good Proof™ matters because it reduces the most expensive part of modern AI operations:

the argument afterwards.

When a decision can affect a customer, a claim, a premium, or a complaint outcome, speed is useful.

But provable reliance is what makes speed usable.

That is the layer institutions will pay for now and rely on later.

Good Proof™ Resources For Buyer And Technical Review

For teams evaluating this now, the next step should feel like due diligence, not a leap of faith.

Buyer Review Paths

Responsible AI and governance buyer guide

Claims and complaints buyer guide

Risk and assurance buyer guide

Procurement buyer guide

Data protection and information governance buyer guide

DORA and third party resilience buyer guide

Technical Review Paths

Insurance sector overview

Verify API

Stamp specification

Specimen Status Link (live validity example)

IDA Evidence Pack specification

Clause pack (procurement and control language)

Next Step

Book an Insurance Stamp Sprint

See stamped specimens

Request a policy workshop (scope and control design)